The 3-Minute Rule for Auto Insurance Agent In Jefferson Ga

Wiki Article

Home Insurance Agent In Jefferson Ga Fundamentals Explained

Table of ContentsLife Insurance Agent In Jefferson Ga - The FactsInsurance Agent In Jefferson Ga Fundamentals ExplainedThings about Home Insurance Agent In Jefferson GaThe Best Strategy To Use For Insurance Agent In Jefferson Ga

Discover more about just how the State of Minnesota sustains active duty members, professionals, and their families.

Term insurance policy supplies defense for a specified amount of time. This duration could be as short as one year or supply protection for a details number of years such as 5, 10, two decades or to a specified age such as 80 or in many cases as much as the oldest age in the life insurance coverage death tables.

If you die throughout the term duration, the company will certainly pay the face quantity of the plan to your recipient. As a guideline, term plans provide a death advantage with no cost savings aspect or cash worth.

Auto Insurance Agent In Jefferson Ga - The Facts

The premiums you pay for term insurance policy are reduced at the earlier ages as contrasted with the premiums you spend for irreversible insurance policy, yet term rates climb as you grow older. Term plans may be "exchangeable" to a permanent strategy of insurance. The insurance coverage can be "level" supplying the very same advantage until the policy expires or you can have "lowering" coverage during the term period with the costs remaining the same.Currently term insurance coverage rates are extremely competitive and among the least expensive traditionally skilled. It should be kept in mind that it is a widely held belief that term insurance policy is the least pricey pure life insurance policy protection offered. https://papaly.com/categories/share?id=ccf6327c00c3463f8ddae1e363e10f4d. One needs to assess the plan terms meticulously to choose which term life alternatives appropriate to satisfy your certain situations

The size of the conversion duration will differ depending on the kind of term policy acquired. The costs price you pay on conversion is usually based on your "present attained age", which is your age on the conversion date.

Under a level term policy the face amount of the policy remains the very same for the whole period. With reducing term the face amount decreases over the duration - Home Insurance Agent in Jefferson GA. The costs stays the very same each year. Frequently such plans are offered as home loan security with the quantity of insurance lowering as the equilibrium of the mortgage decreases.

The Greatest Guide To Business Insurance Agent In Jefferson Ga

Typically, insurance firms have actually not deserved to change premiums after the plan is sold. Since such plans may proceed for years, insurers have to utilize conventional mortality, rate of interest and expense price quotes in the premium estimation. Flexible premium insurance, nonetheless, enables insurers to offer insurance coverage at lower "existing" premiums based upon much less conservative assumptions with the right to transform these premiums in the future.

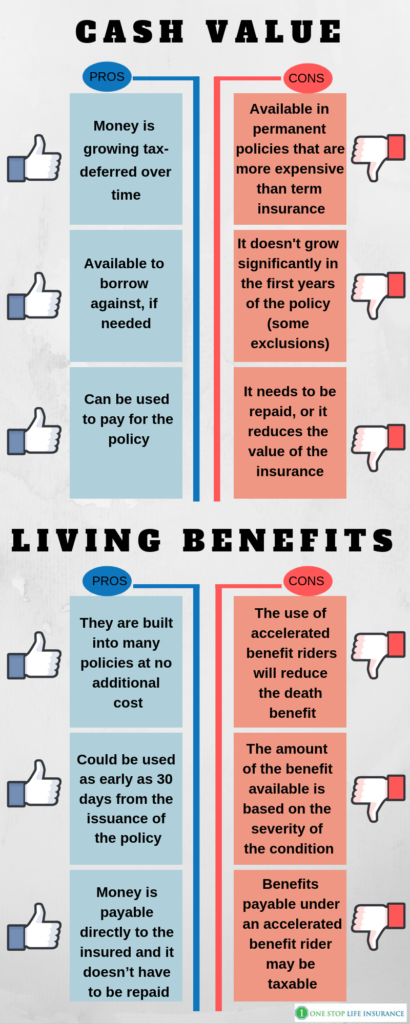

Sometimes, there is no connection in between the dimension of the cash value and the premiums paid. It is the cash worth of the policy that can be accessed while the insurance policy holder lives. The Commissioners 1980 Requirement Ordinary Mortality Table (CSO) is the present table utilized in computing minimum nonforfeiture values and policy books for regular life insurance policies.

The plan's important aspects contain the premium payable every year, the survivor benefit payable to the beneficiary and the cash surrender value the insurance policy holder would receive if the policy is surrendered prior to death. You might make a car loan versus the money worth visit this page of the plan at a specified price of interest or a variable rate of interest yet such superior finances, otherwise paid back, will minimize the survivor benefit.

Auto Insurance Agent In Jefferson Ga - Truths

If these price quotes alter in later years, the firm will certainly change the costs as necessary but never ever over the optimum guaranteed costs specified in the policy. An economatic entire life plan attends to a basic amount of getting involved whole life insurance policy with an extra supplemental insurance coverage given via the use of rewards.

Ultimately, the returns additions should equate to the initial amount of supplementary protection. Since rewards may not be adequate to acquire enough paid up enhancements at a future day, it is possible that at some future time there might be a substantial reduction in the quantity of extra insurance policy coverage - https://www.bark.com/en/us/company/alfa-insurance---jonathan-portillo-agency/gz9nP/.

Since the premiums are paid over a shorter span of time, the costs settlements will certainly be greater than under the whole life plan. Single premium whole life is limited repayment life where one large premium payment is made. The plan is fully compensated and no more costs are required.

Report this wiki page